Let me tell you something, I wish someone had explained to many migrants before they got their first UK payslip.

The salary you agree to when you accept a job is not the same amount that enters your bank account.

It sounds obvious once you understand it, but for many people, that first payslip can be confusing. You might see deductions you didn’t expect, numbers that don’t match the salary you were offered, and unfamiliar terms that make everything feel more complicated than it should be.

I’ve seen people panic, thinking their employer made a mistake or that something went wrong with payroll. In reality, nothing is wrong. It’s simply how the UK salary system works.

Once you understand what’s happening on your payslip, everything becomes clearer, and planning your finances becomes much easier.

So let me walk you through it the same way I’d explain it to a friend.

The Salary You Agree To Is the Starting Point

When you apply for jobs in the UK, employers usually advertise salaries as an annual figure.

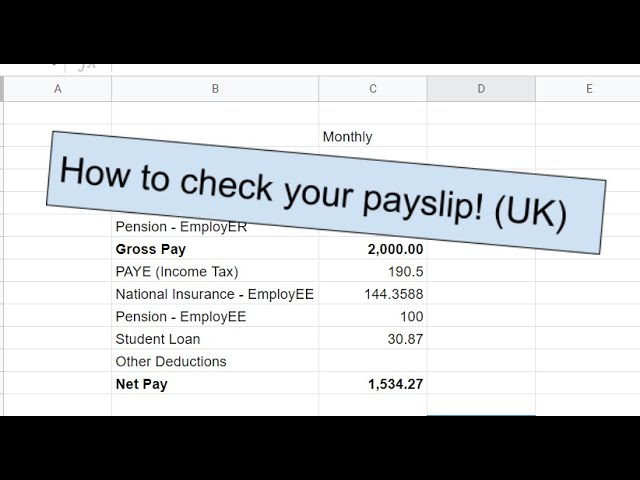

You might see something like £30,000, £38,000, or £45,000 a year. This number is called gross salary.

Gross salary is the total amount you earn before any deductions are taken out. It’s the number used in your job offer, employment contract, and negotiations.

But here’s the key thing to remember: gross salary is not what you’ll actually spend each month.

Think of it as the headline number, the starting point before taxes and other contributions are removed.

Your real spending money is called net pay (often called take-home pay), and that’s the amount that finally reaches your bank account.

Understanding the difference between those two numbers is the first step to making sense of your payslip.

Income Tax Is Deducted Automatically

One thing that surprises many migrants is how taxes are handled in the UK.

In some countries, people calculate and pay taxes themselves throughout the year. In the UK, the system is designed to make things simpler for employees.

Taxes are usually deducted automatically through a system called Pay As You Earn (PAYE).

This means your employer calculates your tax and sends it directly to HM Revenue & Customs before your salary even reaches your account.

You don’t need to manually transfer money or remember monthly payments; the system handles it for you.

How much tax you pay depends on several factors, including your salary level and your personal allowance, which is the amount you can earn before paying income tax.

Once your tax code is set correctly, the PAYE system ensures that tax deductions happen smoothly each time you’re paid.

National Insurance Is Another Deduction

Now here’s another line you’ll almost certainly see on your payslip: National Insurance.

At first glance, many people assume it’s just another form of tax. But technically, it’s different.

National Insurance contributions help fund things like the UK state pension and certain social benefits. It’s a system designed to support long-term social services.

Even though it’s separate from income tax, it’s still deducted from your salary automatically.

For many employees, the combination of income tax and National Insurance accounts for the biggest difference between their gross salary and their take-home pay.

This is usually the moment when new migrants realise why their bank deposit looks smaller than they expected.

But once you understand where the money is going, it becomes easier to accept and easier to plan around.

Workplace Pensions Also Affect Your Payslip

Another common deduction that surprises people is the workplace pension.

In the UK, most employees are automatically enrolled into a pension scheme through their employer. This system is designed to help people save for retirement gradually over time.

A small portion of your salary is deducted and placed into your pension fund. The good news is that your employer also contributes money to the same fund.

So while it reduces your immediate take-home pay slightly, it’s actually building savings for your future.

Many people choose to stay enrolled because it’s essentially free money added by the employer. Others may adjust their contribution levels depending on their financial situation.

Either way, it’s important to recognise that pension deductions are part of the long-term financial structure in the UK.

Why Two People With the Same Salary May Take Home Different Amounts

Here’s something that confuses people all the time.

Two colleagues can earn the same salary but receive different amounts in their bank accounts each month.

At first glance, that seems unfair or suspicious, but there are usually simple explanations.

Several factors can affect someone’s net pay, including:

• Their tax code

• Pension contribution levels

• Student loan repayments

• Benefit deductions

• Additional allowances

Because everyone’s financial situation is slightly different, their deductions can also differ.

This is why comparing payslips with friends or coworkers rarely gives you the full picture. The numbers might look similar on paper, but personal circumstances change the final result.

Why Understanding Your Payslip Gives You Control

Once you understand how deductions work, your payslip stops feeling mysterious.

Instead, it becomes a tool that helps you manage your finances properly.

You can see exactly how much tax you’re paying, what you’re contributing to your pension, and how much money you actually have available each month.

That clarity makes budgeting easier.

It also helps you avoid one of the most common financial mistakes migrants make: planning life based on gross salary instead of take-home pay.

My Honest Advice for Planning Your Life in the UK

If I were advising a friend moving to the UK, I’d say this:

Always build your budget around take-home pay, not your gross salary.

When you know exactly what arrives in your bank account each month, it becomes much easier to plan rent, transport, food, savings, and everything else.

The UK financial system can feel confusing at first, especially if it’s different from what you’re used to. But once you understand how payslips work, things start to feel much more predictable.

And when your income becomes predictable, your financial decisions become much calmer and more confident.

Clarity around your payslip doesn’t just explain your salary, it helps you take control of your money.

Leave a Reply